the Editor says: Dive insurance has been mentioned ever since Open Water Diver training, but honestly, almost every time I head overseas or dive locally, I have no idea whether the dive shop has arranged any coverage for us. International DAN always feels out of reach — the fine-print policy terms are a nightmare for my aging eyes, and the premiums aren't cheap either. My biggest fear is paying for coverage only to discover, when something actually goes wrong, that it doesn't apply in Taiwan at all. Fortunately, I have a friend who both dives and knows insurance inside and out — so of course I had to pick her brain!

After we shared this topic it generated a huge response. We'd also like to thank the long-term Taiwan DAN support team for providing feedback and sharing their hands-on experience assisting DAN's operations in Taiwan. We hope this helps everyone develop a deeper understanding of dive safety!

Scope of Dive Insurance:

Scuba diving is a high-risk sport. Beyond ordinary physical injuries, there is the more serious matter of decompression sickness (DCS) treatment. According to a friend who once worked as an instructor in the Maldives, someone he knew underwent hyperbaric chamber treatment — three sessions came to roughly NT$200,000, and that didn't even include medical evacuation costs. Understanding how to use existing insurance plans to reduce financial risk is therefore something every diver should know.

If we run through just a few scenarios, it becomes clear that all kinds of small mishaps can occur during a dive trip that insurance can help cover: common ones include throwing out your back lugging gear, tripping and falling, getting stung in the face by a jellyfish, or being bitten by a fish; more serious events include nitrogen narcosis from diving too deep, decompression sickness (DCS) from staying down too long, or a week-long hospital stay before you can go home. All of these can fall within the scope of insurance coverage. To choose the right plan for yourself, you first need to understand what each plan actually covers.

What Is DAN:

When talking about dive insurance, we must start with DAN — a name familiar to every diver. DAN is not a commercial organisation; it is a non-profit organisation, and it operates through different regional branches for different parts of the world. Below we focus on DAN Asia-Pacific, which is the branch most commonly encountered by divers in Asia. All information is excerpted from the DAN Asia-Pacific official website. If there is any lag in updates due to timing, please refer to the announcements on the DAN website as the authoritative source.

- DAN Asia-Pacific is an independent non-profit organisation headquartered in Melbourne, Australia.

- DAN is not owned by any training agency, corporation, or shareholders — it is an association.

- Accident & General Insurance Company, Ltd. (hereinafter "AGI") has issued a group diving accident insurance policy (hereinafter the "Group Policy") to Divers Alert Network (DAN) Asia-Pacific Limited.

- Coverage is available to any recreational diver or snorkeler who holds a DAN Asia-Pacific membership and is at least 12 years of age — including instructors and Divemasters supervising recreational diving activities, as well as some research divers and underwater photographers. Commercial diving activities outside of the above are not covered.

DAN Fee Summary & Comparison:

TravelAssist membership: includes worldwide emergency evacuation coverage, 24/7 medical support, access to member-exclusive value-added programmes, and more. Annual fee: AUD 75.

Membership + optional diving treatment coverage:

- Membership + Leading Benefits = AUD 170.

- Membership + Premier Benefits = AUD 224.

DAN Advantages (the following analysis reflects subjective opinions — take as suits your personal preference):

- DAN is international in scope, with service points in countries around the world — highly suitable for divers who travel overseas frequently.

- In the event of an emergency medical need, DAN TravelAssist can provide coordination and evacuation services, reducing overall medical expenses.

- High coverage amounts reduce the financial pressure when an accident occurs.

Things to Understand Before Purchasing DAN (the following analysis reflects subjective opinions — take as suits your personal preference):

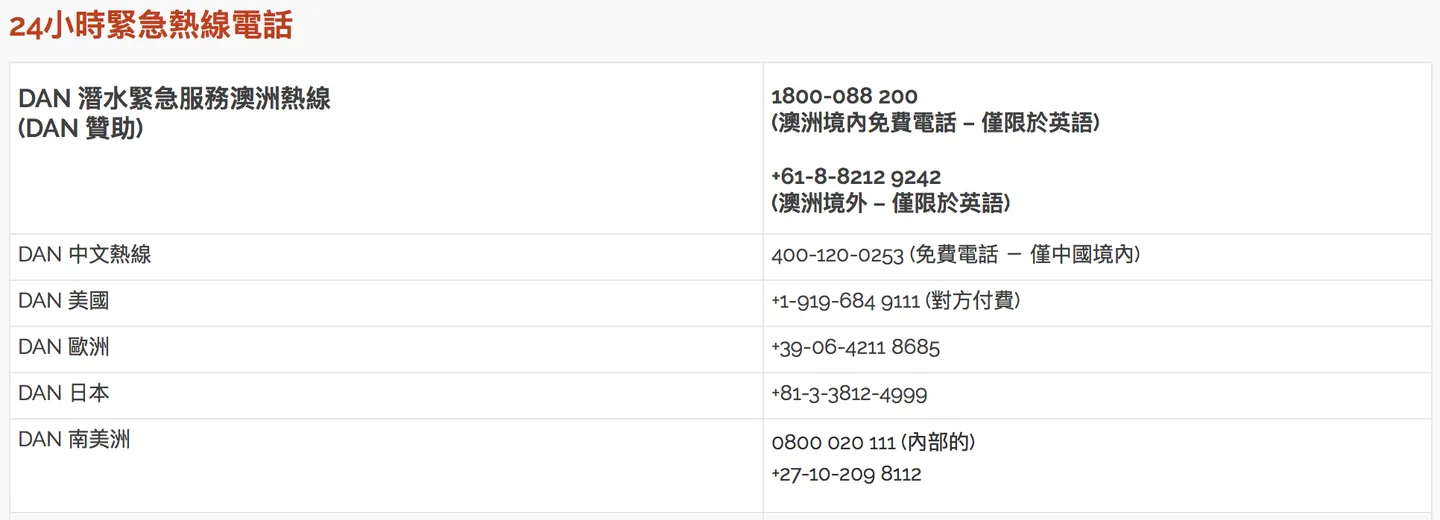

- When a medical incident unfortunately occurs, you need to call the Australian office or another regional branch. There is no DAN office in Taiwan; the nearest 24-hour service hotline is the China line. TravelAssist requires calling the US DAN TravelAssist office for assistance. Some lines accept English only. (Supplement from Taiwan DAN Support Team, 2018/3/20: When a DAN member has an incident and needs assistance, they must notify the emergency hotline of any DAN global branch as soon as possible. Members who need Chinese-language service may call the Chinese-language line in China. Even when calling an English-language emergency hotline, members may request that the professional on the line arrange for a Chinese-speaking representative to contact them as soon as possible. When calling, members simply need to provide their name, membership number, coverage level, and membership expiry date. Once DAN has confirmed the membership, it will promptly arrange for a Chinese-speaking representative to liaise with the member, understand the situation, and help communicate and coordinate with DAN's English-speaking staff regarding the handling of the incident. For Chinese-language contact, you may also reach out via email: china@danap.org.)

- DAN plan insurance operates as secondary insurance — after other insurance has paid out, the DAN Asia-Pacific plan will cover 100% of the remaining eligible medical expenses. In other words, if you hold a related policy with a Taiwanese life insurance company, the Taiwanese insurer's payout must first be deducted before DAN steps in to cover the remainder. (Supplement from Taiwan DAN Support Team, 2018/3/20: In general, DAN members use DAN coverage as their primary insurance, because the scope and amounts covered for emergency medical evacuation and medical expenses are usually sufficient to cover evacuation, transport, and medical costs arising within one year of an incident — there are very few cases where a DAN member needs another insurer's coverage to supplement a shortfall. If a DAN member chooses to use another insurer's coverage as the primary payer and that coverage proves insufficient to meet the costs and expenses arising from the incident, the member's DAN coverage can then step in as supplemental support to make up the difference.)

- Claims require the submission of English-language documents, and the document review period can be lengthy. (Supplement from Taiwan DAN Support Team, 2018/3/20: The insurance companies providing DAN member coverage are all foreign companies, so the claims documentation required is naturally primarily in English. However, because DAN's service area spans more than 130 countries worldwide, not all regions use English as their primary language. After an incident occurs, DAN members may submit all receipts and supporting documents — even those in languages other than English — together to their DAN branch when filing a claim. DAN staff will forward these to professional translators before submitting them to the insurance company for processing.)

Other Insurance Options:

In addition to DAN's insurance plans, there is no need to look far afield — Taiwan's own life insurance companies also offer relevant services worth exploring. Among Taiwanese insurance plans discussed in relation to diving, the one most commonly talked about is Fubon Property & Casualty Insurance's "Vibrant Life" Comprehensive Insurance, which is primarily designed for outdoor sports enthusiasts to use as a supplementary plan. Note the emphasis on supplementary — we'll explain shortly how to combine plans for the most cost-effective coverage. All information below is subject to the announcements on the Fubon Property & Casualty "Vibrant Life" Comprehensive Insurance website.

Travel Accident Insurance?

Is Fubon's "Vibrant Life" Comprehensive Insurance the same as the travel accident insurance (旅平險) we often hear about? We use the table below to give a brief overview. In short, standard travel accident insurance generally does not cover decompression-related illness that may arise from diving, whereas the "Vibrant Life" Comprehensive Insurance explicitly states that decompression treatment is within its coverage scope.

[caption id="attachment_2885" align="aligncenter" width="1268"] Fubon Official Website[/caption]

Fubon Official Website[/caption]

Premium Calculation:

Fubon Life's "Vibrant Life" Comprehensive Insurance first divides coverage into two categories of specified activities. Category 1 includes paragliding (hang gliding), powered paragliding, parasailing, skydiving, rock/ice climbing, equestrian sports, martial arts competitions, and scuba diving; Category 2 covers camping, cycling, road running, hiking, and other activities not listed under Category 1. Premiums are then calculated based on the plan you choose (taking into account age and number of insured days).

For example: a 30-year-old diver planning a 5-day dive trip, choosing Plan 4, would pay a premium of NT$789. The table also illustrates that scuba diving — classified under Category 1 — is assessed by insurers as a high-risk sport (under identical conditions, Category 1 costs NT$789 versus NT$411 for Category 2).

[caption id="attachment_2886" align="aligncenter" width="1194"] Fubon Official Website[/caption]

Fubon Official Website[/caption]

What about the international medical services that divers care about most? This plan also provides an SOS overseas emergency assistance hotline, with a maximum compensation per incident of US$10,000.

Fubon "Vibrant Life" Advantages (the following analysis reflects subjective opinions — take as suits your personal preference):

- Customer service hotline provides Chinese-language support (goes without saying!), and there are plenty of Fubon insurance agents nearby to consult.

- Priced by the day, allowing you to design the insurance plan that best fits your needs.

- Domestic Taiwan claims are processed the same way as any standard insurance claim — no need to specifically prepare English-language documents or mail anything overseas.

Combine Your Travel Insurance for a Worry-Free Trip Abroad!

By simply pairing the travel accident insurance and travel inconvenience insurance commonly used for overseas trips, you can achieve comprehensive coverage for virtually every mishap that could occur on a dive trip — from minor issues like flight delays and lost luggage, to more serious events like overseas medical treatment and decompression sickness (DCS) treatment — giving you complete peace of mind on your dive travels.

Conclusion!

- DAN offers substantial coverage amounts and comprehensive overseas support, but there is no local on-the-ground service in Taiwan. It is recommended for divers who take 3 or more overseas dive trips per year (or those heading to more unusual dive destinations such as the Galápagos or ice diving).

- Fubon Property & Casualty travel accident insurance + "Vibrant Life" Comprehensive Insurance can be tailored to your actual needs and covers all likely risks on a dive trip, with local service that minimises the hassle of communication and document submission.

[caption id="attachment_2887" align="aligncenter" width="980"] Dive happy — safety is the one thing that always comes first[/caption]

Dive happy — safety is the one thing that always comes first[/caption]

Special Thanks:

Special thanks to Alice from the "Let's Dive" classmates group for sharing her insurance knowledge. She is herself a passionate underwater conservation diver. If anyone has questions about dive activity insurance, feel free to reach out to her!

- 林微錚 0937-995972

- undertheseaalice@gmail.com

- LineID:@559CLJCZ